Getting the basics of digital customer onboarding in the banking sector right

Publish Date: May 17, 2021Design a customer-centric solution based on empathy and customer psychology

The surging numbers of ‘digital only’ customers have been increasingly making their mark in the banking sector. Digital Transformation has been setting new modus operendi for customer service across a large fraction of banking functionalities.

However, few areas like customer onboarding largely remained cocooned with traditional face-to face interactions. One of the key factors to reserve this first customer touch point with physical interactions, was to build stronger emotional attachment, gain trust and nurture a long-standing relationship with the customers.

This theory, in the long-run, however proved fallible. The emergence of challenger banks with their end-to-end digital service, further posed a threat to the traditional onboarding practice.

However, the changing digital dynamics in banking doesn’t nullify the initial logic that physical interactions ease interpersonal relationship with customers. According to the, the digital-only banking customers are less satisfied than their branch-only counterparts. Replicating an interpersonal yet seamless experience with focus on speed, standardization and simplicity is no easy feat in a digital environment.

As the banks were caught in the conundrum of whether to digitize customer onboarding or not, the COVID 19 pandemic acted as a catalyst thrusting the banks towards the inevitable. Banks could no longer procrastinate from embracing a full-scale digitalization. Today, the top three questions that I encounter from the digital heads at banks are:

- How to reduce the complexity of design and navigation in order to provide a seamless online onboarding experience?

- How to control the increasing vulnerability to cybercrime and ensure privacy and security to customers?

- How to ensure a strong digital interpersonal relationship to ensure long-term customer allegiance?

While I attempt to address these questions in the next section of the blog, let us also take into account some of the common reasons of failure by the early entrants:

- Complex online process emulating the on-ground process

- Partial digitalization making customer visits to branches mandatory

- Paper-based identification process

- Collection of too much and repetitive information

- Failing to adhere to legal / regulatory compliance

- Lengthy navigation leading to higher abandonment rate

- Low level of success across multi-channels

Getting the basics right:

1. Use design thinking to create a simple, short and seamless account opening process

The concept of ‘going digital’ does not mean emulating the traditional onboarding processes in a digital platform. It is not transferring the lengthy, complicated paper-based forms in a web or mobile interface. It is not creating duplication of verification efforts for customers across online as well as physical branch visits.

It is to apply a customer-centric design approach based on empathy and understanding of customer psychology. An approach that is proved simple, short and user-friendly through multiple prototyping and tests. Some effective principles include:

- Keeping the whole onboarding process under 5 minutes.

- Keeping questions to a minimum and avoid repetition.

- Inform customers why data is required and how it is used to gain their confidence.

- Introduce Smart eForms with guided-snippet based flow, supported by automation to reduce data entry.

- Introduce Self-service models to empower customers towards quick self-resolutions of specific problems

- Automated information saving functionality to give customers the option to drop out in the middle of filling a form and restart at their convenience.

- Simplify ID collection and authentication process that is mobile optimized for instant submission and automated approval.

- Easy and automated validation.

- Introduce eSignatures as legally binding customer consent.

- Creating electronic ID and secure log in to optimize engagement during a customer lifecycle.

2. Design a mobile first and integrated omnichannel experience

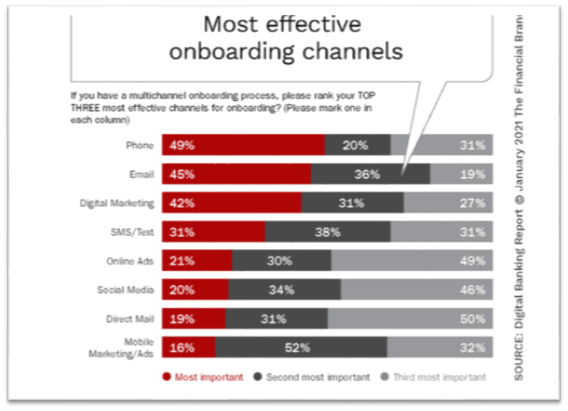

The ubiquity of smartphones has made mobiles the primary choice for anywhere and anytime access. Indisputably it has become the most effective onboarding channel as corroborated by The Digital Banking report January 2021 study.

It is therefore fundamental for banks to design a 100% mobile solution for onboarding as well. Technology advancements enable end-to-end onboarding through mobile phones. With an intuitive design, mobile onboarding can be a seamless experience without any breakpoints in the customer journey such as printing, signing, or uploading and emailing supporting documents and identification.

Besides providing a mature mobile experience, banks should aim at delivering a fully integrated omnichannel experience across other channels like social, PC, laptops, tablets as well. Merging all customer interaction channels into a single channel ensures faster customer response and higher conversion rate.

3. Cyber-security and compliance

While digitalization on one hand opens a new world of opportunities, it increases the vulnerability towards cybercrimes which is growing at an even alarming rate with the virtual work-from-home norms. Specially for financial institutions and banks who are dealing with critical KYC data, it is imperative to embed high-end security features to gain trust of the customers with regards to privacy and data protection.

Banks should be proactive in designing a comprehensive and modern governance, risk, and compliance models that effectively respond to all existing as well as upcoming compliance requirements, for onboarding and more. Some of the key steps include:

- Performing an automated match between an ID card and a national ID database

- Deployment of modern technology, such as, facial recognition to verify liveness detection

- Blacklist check

- Anti-money laundering (AML) check

- Integration with the credit bureau to validate the customer identity

Relying on expertise of YASH Technologies to take care of the intricacies of the ever-changing regulatory policies across different countries will help banks adopt to a platform that integrates the various systems and avoid high penalties for non-compliance.

Disregarding customer engagement will have a long-term impact that cannot be overturned. While embracing digital onboarding, banks should reassess their depth of customer communication, personalized service recommendations, timely engagement, and multichannel integration. Some quick tips of ensuring quality engagement include:

- The provision to engage with local branch staff for quick resolution.

- Offer customized service in lieu of the standard one-size-fit all service by creating an individual customer journey graph.

- Facilitating real-time collaboration with service reps enabling them to guide customers in distress over phone while simultaneously viewing their screen for quick resolution.

The pandemic has accelerated the pace of digitalization pushing banks beyond their traditional boundaries. While the digital heads at banks should concentrate on product innovation and financial service offerings, the true value proposition will be determined in the experience they offer during customer acquisition. We at YASH are here to help you reimagine your account opening process, integrate seamlessly with your IT systems and make your customer onboarding future ready. Don’t miss my next blog on the ‘key steps to building architecture of digital customer onboarding’.

Reimagine how you deliver value when onboarding banking prospects with a single digital platform, explore our services more.

More From Author.

Related Posts.

AWS Cost Optimization Tips

Pravish Jain

Why one should adopt DataOps?

Pravish Jain

Multicloud strategy

Pravish Jain

Hybrid Environment – Gotchas

Pravish Jain